US stocks are approaching a record high and the outlook for Corporate America is only expected to brighten. Now investors are waiting to see if the Federal Reserve derails the market’s bull run.

Amid signs that inflation pressures are finally ebbing, setting up what has historically been a bullish stretch, the S&P 500 Index is a mere 5.4% below its all-time peak. It’s a backdrop that raises the stakes for this week’s pivotal central bank meeting, with economists still debating whether a recession is ahead this year.

The danger, of course, is that a resilient labor market pushes policymakers to signal further tightening beyond this week’s expected rate hike, jeopardizing Wall Street’s profit forecasts, especially for the high-flying tech shares that have been key to this year’s advance.

“The risk is if the Fed feels compelled to reaccelerate the tightening cycle,” said Ed Clissold, chief US strategist at Ned Davis Research. “If that’s the case, it could end up being the policy mistake that everyone was looking for.”

Investors are bracing for a massive week on two fronts. Around 170 companies in the S&P 500, accounting for some 40% of its market capitalization, are scheduled to report earnings, including bellwethers Microsoft Corp., Meta Platforms Inc. and Google parent Alphabet Inc.

Read More: Netflix, Fed Cast Clouds Over Tech-Stock Surge: Earnings Watch

And yet Wednesday may prove decisive, with the Fed projected to lift its benchmark rate to a 22-year high, followed by Chair Jerome Powell’s press conference. The central bank chief could lean into the chance of an additional hike, a scenario that risks slamming the brakes on growth and upending the bulls.

“I’m positioned defensively because I still think we are headed for a recession,” said Brian Frank, portfolio manager of the Frank Value Fund, who has suggested that investors buy beaten-down energy and utility stocks. “A downturn tends to catch everyone by surprise because people deny it first by calling it a ‘soft landing’ and then we end up with a recession afterward.”

Housing Help

But to Dennis DeBusschere, founder of 22V Research, signs of strength in housing counter the bears’ argument.

US homebuilder sentiment rose in July to the highest level in 13 months. That’s good news for investors awaiting the advance reading of second-quarter gross domestic product this week.

“The most interest rate-sensitive sector, housing, has already stabilized and is a support for GDP growth (mechanically, given the massive housing drag last year),” DeBusschere wrote in a note. “If the most interest-rate sensitive sector is improving, it’s tough to depend on lagged impacts from tightening to justify bearish views.”

The GDP report is projected to show the economy grew at a 1.8% annual clip last quarter, compared with 2% in the prior reading, a Bloomberg survey shows.

On Friday, traders will monitor the employment cost index, a broad gauge of wages and benefits, along with the personal-consumption expenditures price index — the Fed’s preferred inflation measure — which will help determine if the central bank starts favoring another rate increase at its meeting in September.

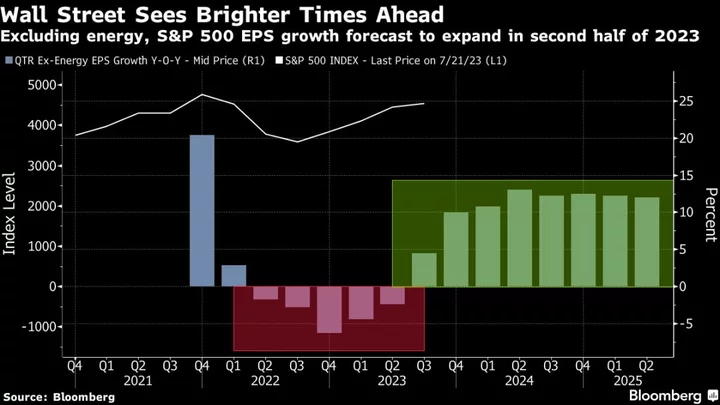

For now, what investors know for certain is the earnings outlook keeps getting better. While profits at S&P 500 firms are forecast to drop for a third straight quarter, earnings are improving when excluding the energy sector, the lone S&P group to have a strong 2022, Bloomberg Intelligence data show. Profit growth without energy is expected to return in the second half of the year, BI data show.

“Earnings have improved considerably relative to what was priced into the stock market late last year,” said Gina Martin Adams, chief equity strategist at BI. “Using the economy as a forecasting tool for the stock market proves to be a really dicey business.”

--With assistance from Norah Mulinda.