The Bank of Japan is widely expected to stick with its negative interest rate this week, leaving the focus on whether it will risk complicating its stimulus message by tweaking its cap on benchmark yields.

Since taking the helm in April, Governor Kazuo Ueda has repeatedly pushed back against the idea that a major pivot on policy is looming by emphasizing his persistent doubts about the sustainability of recent price growth in Japan.

That’s kept the BOJ as an outlier on monetary policy while major peers aggressively hiked rates to tackle hot prices. That divergence looks set to continue with both the Federal Reserve and European Central Bank expected to hike again before the BOJ delivers its decision on Friday — a move which may renew pressure on the yen .

Despite Ueda’s insistence of keeping stimulus in place, price growth in Japan continues to track well above 3%, leaving the BOJ little choice but to raise its inflation forecast for this fiscal year at this week’s meeting. That likely upward revision has helped keep speculation simmering of an adjustment or scrapping of yield curve control.

BOJ officials will likely consider bumping up their 1.8% inflation forecast for this year to around 2.5%, according to people familiar with the matter. An earlier Bloomberg report indicated that officials do not see an urgent need to tweak YCC in July, though they will probably discuss the topic.

“I expect Ueda’s cautious stance will persist against calls for early YCC adjustment,” said Mari Iwashita, chief market economist at Daiwa Securities Co. “The BOJ is still at the stage where it needs to carefully watch for upside inflation risks and downside economic risks.”

Some 82% of 50 economists surveyed by Bloomberg expect the central bank to leave both rates and YCC unchanged for now, with October a more likely timing for change. Still, almost a fifth of those polled, including economists at Goldman Sachs, JPMorgan Securities and BNP Paribas, expect action this week.

What Bloomberg Economics Says...

“We think any tweaks to YCC now would also hurt Ueda’s reputation as a clear communicator; he’s consistently said stimulus is still needed.”

— Taro Kimura, economist

For the full report, click here.

Ueda has repeatedly warned that snuffing out nascent inflation too soon might cause more harm than letting it persist. The governor voted against a premature move to raise rates more than two decades ago, when he was a board member, and is likely keen to avoid a recurrence of going too early.

Economists largely agree that a change to the BOJ’s minus 0.1% short-term interest rate is still a ways off. But there is more debate on when the central bank will adjust or scrap its 0.5% cap on 10-year government bond yields.

By keeping yields low, the bank aims to stimulate economic activity and prices despite bond trader complaints about the market pricing distortion this causes.

Currently, there is no large distortion in the shape of the yield curve at the moment, unlike in December. Benchmark yields have consistently stayed below the BOJ ceiling and the central bank hasn’t had to buy additional bonds to defend its cap for months.

Meanwhile, swap rates have come off their recent highs, indicating some cooling of policy change expectations.

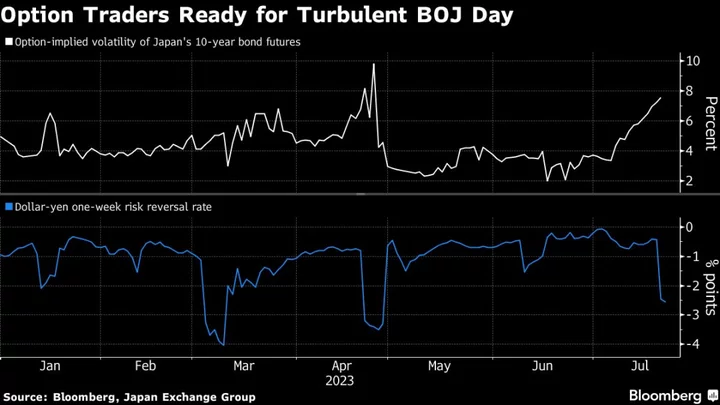

Still, some speculation remains, with some traders opting for just-in-case hedges. Implied volatility in Japan’s bond futures is at a three-month high, signaling a wariness of possible near-term gyrations. An option market gauge of the expected direction of the dollar-yen — so-called risk reversals — suggests traders are guarding against a drop in the pair.

Some analysts argue that the central bank might consider taking an opportunistic chance to tweak YCC when the pressure on the yield cap isn’t so intense.

“We feel the time is ripe to undertake a YCC tweak,” said Aninda Mitra, head of Asia macro and investment strategy at BNY Mellon Investment Management. “A YCC tweak is not a full-scale pivot to policy tightening. But it sets the stage for reduced policy divergence.”

Such a move would ease pressure on the yen, modestly bump up benchmark yields toward 1% and remove distortions in the bond market, he said. If the BOJ doesn’t move this week, investors should consider every subsequent meeting this year as live for possible YCC changes, he added.

Speculators focusing on possible YCC tweaks are missing the more important point of how and when the BOJ will feel confident about achieving its 2% inflation target, former BOJ deputy governor Masuzumi Wakatabe said on Bloomberg TV. That presents the bank with a communications challenge, the Waseda University professor added.

“Market participants are kind of focusing on the details rather than the main message,” Wakatabe said.

--With assistance from Daisuke Sakai, Masaki Kondo, Kathleen Hays and Yumi Teso.