The craze for fast-expiring options is ramping to unprecedented heights in a stock market that has lately been given to severe intraday moves. It’s probably not a coincidence.

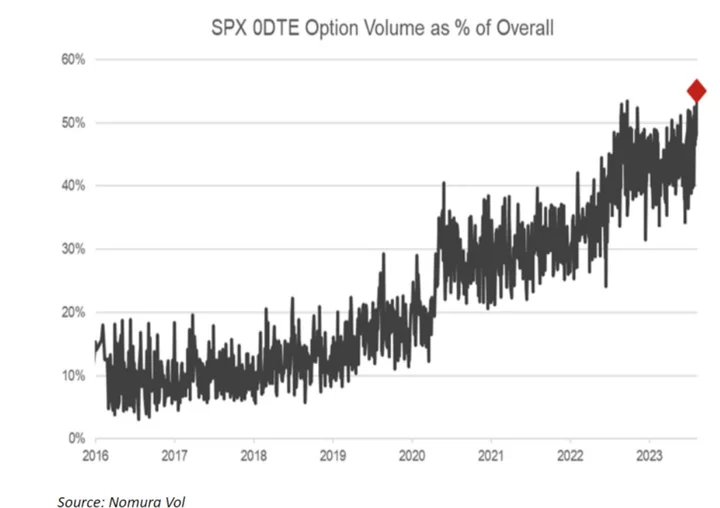

About 1.86 million so-called zero-day contracts — those tied to S&P 500 with a maturity less than 24 hours — changed hands on Thursday, making up a record 55% of the index’s total volume, according to data compiled by Nomura Securities International. Halfway into August, the options known as zero days to expiration, or 0DTE, have seen four of their top 10 most-traded sessions ever.

Their mushrooming popularity coincides with a shift in the market’s backdrop that has made tools for fleeting speculation more tempting. Over the last two weeks, S&P 500 futures have wiped out gains of at least 0.9% in separate sessions, a break in the upward momentum that had carried the index 28% higher over 10 months.

The intraday selloffs have “driven a behavioral change in 0DTE space vs what we have seen largely during the rally,” said Charlie McElligott, Nomura’s cross-asset strategist. “It’s an environment ripe for 0DTE trading swings, ranges or overshoots as the perfect vehicle. But then too, it’s feeding such moves.”

Befitting their reputation as tools for quick bets, 0DTEs saw two of their heaviest sessions occur when major economic data were published: monthly payrolls on Aug. 4, and the consumer price index on Aug. 10. Traders may have taken advantage of low-cost options to position around these events, said Stuart Kaiser, head of US equity trading strategy at Citigroup Inc.

Also notable has been a turn in the type of options traders have favored — from bullish to bearish. Over the past 20 days, puts outnumbered calls by almost 10%, according to data compiled by Kaiser. That’s a departure from the previous two months, when flows were dominated by calls.

“You could argue with implied volatility low, the 0DTE options are an alternative to trading equity futures tactically,” he said.

How derivatives interact with their underlying assets is the subject of extensive academic scrutiny. The boom in zero-day options since last year has sparked an intense debate on Wall Street about whether the popular trading tool has the potential to influence — or even destabilize — the $47 trillion American equity landscape.

Normua’s McElligott observed that the market has experienced greater intraday tumult of late, with gains or losses frequently reversing in a way that — ironically — leads to more subdued moves on a close-to-close basis. Last week, for instance, the S&P 500’s high-low swing averaged 0.9%, 2.2 times its daily move on a closing basis. That compared with a ratio of 1.6 in the first seven months of the year, data compiled by Bloomberg shows.

The surge of 0DTE options, he says, may have played a role in the gyrations. Fueling such dynamics are market makers who are on the other side of options transactions and need to buy or sell stocks to maintain a market-neutral stance, a process known as gamma hedging. Recently, they’ve turned “short gamma,” a stance obliging them to go with the prevailing market trend, selling stocks when they go down, or vice versa.

Theoretically, that may give zero-day options an ability to impose an outsize influence on the broad market when they’re initiated. Given the recent pivot toward put buying from traders, that could add fuel to intraday selling. Yet once these positions expire near the session’s close, market makers may need to unwind their hedge, causing a turnaround in stocks.

That’s what happened last Friday, when many at-the-money puts turned profitable for their holders and the S&P 500 bounced from the session’s low, according to Nomura’s McElligott.

“They closed those puts by the end of day to monetize and that’s what rallied us back,” he said. “That was more of the same 0DTE vol suppression phenomenon because they either expire worthless majority of time, or if in money, you get a reversal impulse when monetized by close.”