Embattled Swedish landlord SBB is facing an inflection point after Fir Tree Partners demanded its money back, according to a person familiar with the matter. This marks the first such written notice for the property company.

The New York-based hedge fund sent a letter to Samhallsbyggnadsbolaget i Norden AB — as the firm is officially known — saying it was in breach of a key debt term, said the person who asked not to be identified because they’re not authorized to speak publicly about it.

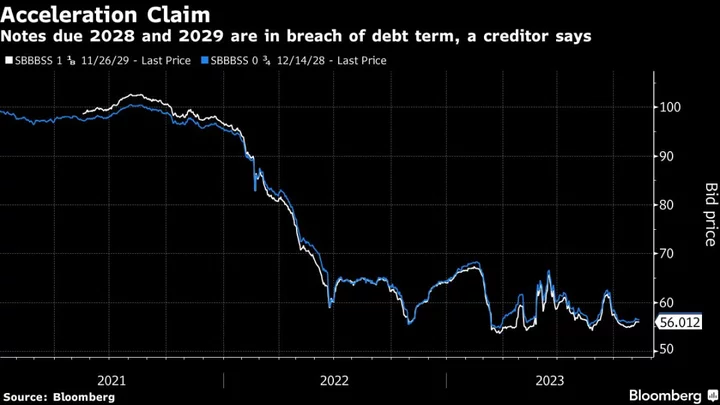

The holdings in question total about €46 million ($49.2 million) in the two series of euro-denominated social bonds, which correspond to about 1% of SBB’s total bond stock, according to a statement by SBB late on Thursday.

An email requesting comment was sent to Fir Tree on Friday outside of US working hours. SBB declined to comment on the identity of the bondholder.

SBB remains at the center of Sweden’s property crisis as landlords scramble to find ways to refinance billions of dollars of bonds amassed in the cheap-money era. Now one of those bondholders has run out of patience, saying repayment is needed on the grounds SBB breached a key term in its debt.

The pressures now being felt among borrowers such as SBB and Heimstaden Bostad AB underscore the depth of Europe’s unfolding real estate crisis, with companies like Signa Holding GmbH teetering on the brink. In Sweden, much of the bond debt is floating rate and short term, which is why the squeeze from higher interest rates has hit the country first.

SBB’s creditor sent a letter to the company claiming the landlord had breached a threshold measuring the amount of profit divided by the interest owed on its debt — known as the interest-coverage ratio — and as a result the company must immediately repay the notes ahead of their scheduled maturity in 2028 and 2029, according to the statement.

SBB said it “firmly rejects” the claim that it is in breach “and as such considers that the acceleration notice received from this Eurobond holder is ineffective.”

“The debt held by those making these claims is a very small fraction of our outstanding debt,” said Chief Executive Officer Leiv Synnes in an interview.

This development comes in the wake of a major reorganization at SBB, announced by Synnes in September, to split the company into three units and secure fresh funds to cover a near-term funding gap of about $730 million. Despite taking a major step toward stabilizing its finances, the group’s bonds have continued to trade at deeply distressed levels while its share price has languished near record lows.

The CEO, who declined to give the names of those making the claim, told Bloomberg that “the issue itself is not a new one, similar opinions have been voiced previously and we made our position clear already in May.”

Earlier this summer a group of bondholders, advised by PJT Partners, demanded that SBB make a number of changes at the company. The group warned at the time that “a signification portion” believed the landlord had breached the interest-coverage covenant and would push for an event of default if progress wasn’t made quickly enough.

Read More: Embattled SBB Hit With Bondholder Demands as Pressure Mounts

“It’s in SBB’s and all our stakeholders’ best interest to allow the company to continue to execute on its strategy and strengthening its financial position,” Synnes said.

The Stockholm-based landlord had been due to report earnings for the third quarter today, but earlier this week pushed back the publication date to Monday, Nov. 13.

--With assistance from Jonas Ekblom.

(Adds context)