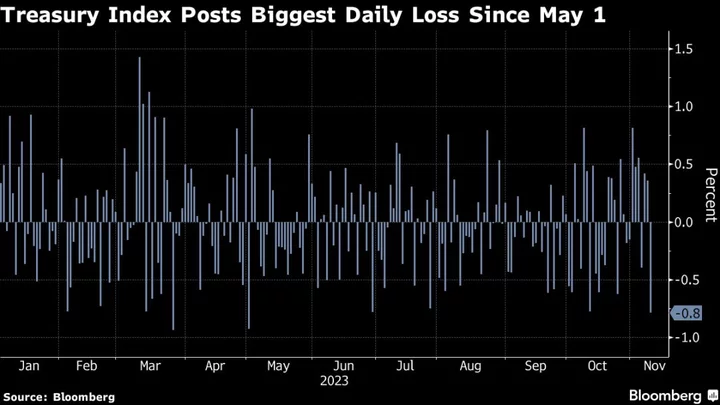

For a moment this week, the brutal bear market in US government debt appeared on its last legs. By Friday, concerns about the Federal Reserve and mammoth auction sizes were back in force, underscoring the fragility of any gains.

A disastrous auction of 30-year Treasury bonds Thursday sent long-maturity yields soaring as investors demanded additional compensation for funding a ballooning fiscal deficit. An hour later, Fed Chair Jerome Powell told reporters at the International Monetary Fund conference in Washington that another interest-rate hike aimed at curbing inflation is still possible, unleashing a surge in short-term yields.

As measured by the performance of the Bloomberg Treasury Index it was the worst day in more than six months. Long-dated Treasury yields had reached the lowest levels in more than a month just a day earlier, attributed to investors and traders positioning for the end of the Fed’s historically aggressive tightening cycle.

“It’s still too early to call the all-clear on rates and inflation,” said Alberto Gallo, chief investment officer and co-founder of Andromeda Capital Management. “The Fed might be done hiking, but that doesn’t mean a lot of cuts are coming soon,” as interest-rate futures markets continue to anticipate.

Powell and other Fed policy makers have repeatedly voiced the idea that rising bond yields, by tightening financial conditions, can avert the need for additional interest-rate hikes. From that standpoint, declining yields quickly run into trouble.

Traders continue to see another rate increase as unlikely and to anticipate that the Fed will pivot to cuts next year as the cumulative effect of its hikes since March 2022 takes its toll on the economy. However they priced in a later start — in July, from June — after Powell’s comments.

The bond auction, meanwhile, illustrated that investors aren’t tolerating yield declines well. The market rally that preceded the sale meant that the auction produced a yield of 4.769%, lower than last month’s 4.837% result, which was the highest since 2007.

The auction yield was significantly higher than expected, though, making it one of the worst 30-year bond sales of the past decade. It signified that buyers of Treasuries on the whole are becoming more price-sensitive, a problem for the US government as it seeks to raise larger sums via its auctions.

“What the auction result said is that every one is worried about supply now,” said Mark Nash, head of fixed-income alternatives at Jupiter Asset Management. “Things are changing in the market in terms of support.”

A cyberattack that disrupted trading for clients of the Industrial & Commercial Bank of China Ltd., the world’s largest bank, probably contributed to the poor result, said James Wilson, senior portfolio manager at Jamieson Coote Bonds Pty in Melbourne.

Wilson remains bullish on Treasuries, expecting a reckoning for the US economy.

Still, he said, “after a 50-basis-point rally in the week prior, appetite for the 30-year issue was always going to be questionable.”

Buyers of the auction were rewarded Friday as the new 30-year rallied back in yield terms to around 4.715%, around where it was trading just before the sale for a steep price gain.

“Longer term we’re very bullish on Treasuries and the rates market and we think that they offer really good value,” said Jamie Patton, co-head of global rates at TCW Group, a Los Angeles-based investment firm with about $200 billion under management. “We’ve never, in the history of modern monetary policy, seen the Fed raise rates by over 500 basis points and not had any accident or correction or recession.”

--With assistance from Cormac Mullen.

Author: Anchalee Worrachate, Alice Gledhill, Garfield Reynolds and Ruth Carson