Crypto enthusiasts are hopeful that a once-in-four-years event which rewrites the underlying code of the world’s biggest cryptocurrency will extend the current market rally. But the milestone also risks sounding the death knell for certain Bitcoin miners.

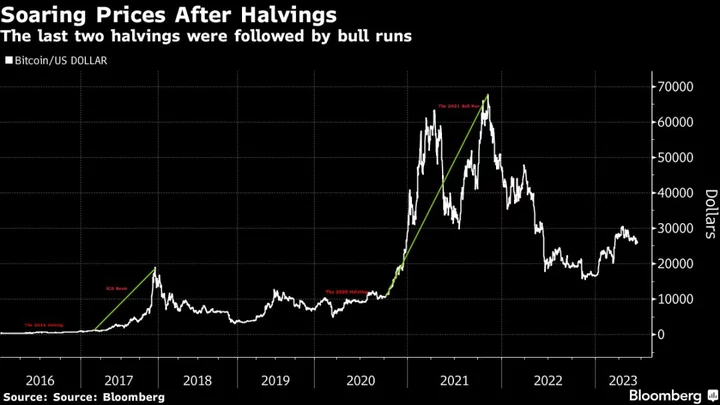

The quadrennial event, rather ominously dubbed “the Halving” or “Halvening,” has historically been followed by exponential surges in Bitcoin’s price. The last three occurrences in 2012, 2016 and 2020 saw the token jump nearly 8,450%, 290% and 560% a year on, Bloomberg data shows. Bitcoin was launched in 2009 by a computer programmer or group of programmers under the pseudonym Satoshi Nakamoto.

Halvings — as the name suggests — slash in half the amount of Bitcoin each miner can earn for validating transactions on the digital asset’s blockchain using specialized, energy-intensive computers. The next halving, slated for April 2024, will cut miners’ rewards to 3.125 Bitcoin per block — or $94,438 — from the current 6.25 or $188,876.

The scarcer supply is seen by crypto proponents as helping to maintain Bitcoin’s value in the long run, or at least until the maximum number of tokens that can ever be mined — 21 million — is reached around 2140. So far, miners have been able to make up for the loss in revenue when the rewards are cut thanks to the rallies in Bitcoin’s price after each halving, as well as technological advancements that have improved the efficiency of their mining rigs.

But mining economics ahead of the next halving look more troubling than previous ones.

“Nearly half of the miners will suffer given they have less efficient mining operations with higher costs,” predicts Jaran Mellerud, crypto-mining analyst at Hashrate Index.

He points to the break-even electricity price of the most common mining machine, which is expected to drop to six cents per kilowatt-hour from 12 cents/kWh after the halving. Around 40% of miners still have higher operating costs per kWh than that, Mellerud said. Miners with operating costs above 8 cents per kilowatt-hour will struggle to stay afloat, as will smaller miners that don’t run their own mining rigs but outsource them instead, he said.

“If you count in everything, the total cost for certain miners is well above Bitcoin’s current price,” added Wolfie Zhao, head of research at TheMinerMag, a research arm of mining consultancy BlocksBridge. “Net profits will turn negative for many miners with less efficient operations.”

Bitcoin has rallied more than 80% this year to around $30,000, though the price is still less than half the record of almost $69,000 reached in late 2021. Meanwhile, miners’ production costs have risen in tandem with electricity prices, and debt burdens have become unsustainable for many of them.

The global mining industry has $4.5 billion to $6 billion in debt — down from $8 billion in 2022 — spanning senior debt, loans collateralized by mining rigs, and Bitcoin-backed loans, estimates Ethan Vera, chief operations officer at crypto-mining services firm Luxor Technologies. Outstanding loans for 12 major public mining companies such as Marathon Digital Holdings and Riot Platforms stood at around $2 billion at the end of the first quarter, down from $2.3 billion in the previous quarter, data compiled by Hashrate Index shows.

The borrowing spate was partly driven by miners migrating to North America from China after the Communist nation’s domestic mining ban in late 2021. “One thing the miners didn’t have is access to the capital market,” said Zhao. “Debt financing is much more available in the US.”

Rising competition among Bitcoin miners has also compressed profit margins. Mining difficulty, a measure of computing power to mine Bitcoin, hit a record high in June, data from btc.com shows. For miners to keep the same profit margins after the halving, Bitcoin’s price will have to rise to $50,000-$60,000 next year, said Kevin Zhang, senior vice president of mining strategy at crypto-mining firm Foundry, which is owned by industry heavyweight Digital Currency Group.

And while miners enjoyed a brief respite earlier this year as Bitcoin’s price rebounded after a long crypto winter and electricity costs fell, power prices are climbing again. Texas, a major crypto hub, is already experiencing an early heat wave.

Bitcoin miners are taking a number of measures to protect themselves ahead of the halving, such as locking in power prices, bolstering war chests and cutting back on investments.

“Coming to the halving itself, miners are preparing by trying to be more sophisticated with their power costs and secure the pricing from their power providers in advance,” said Zhang.

Hut 8 Mining Corp. entered into a $50 million credit facility last month with a unit of Coinbase Global Inc. to help preserve its Bitcoin treasury ahead of the halving. And Texas-based Bitcoin miner Lotta Yotta is shoring up six months’ cash flow while scaling back investments to prepare for the event, according to its CEO, Tiffany Wang.

“During halving year, it is high risk,” Wang said in a text message, referring to additional investment in Bitcoin mining facilities. “It is better to save some fund in the account to keep the company running.”

The halving is ultimately expected to double Bitcoin’s production cost to about $40,000, JPMorgan Chase & Co. strategists led by Nikolaos Panigirtzoglou wrote in a June 1 note. The cost of producing one Bitcoin ranged between about $7,200 to $18,900 in the first quarter across a cohort of 14 publicly-listed miners, data compiled by TheMinerMag shows. The costs calculated don’t include other major expenses like debt interest payments, management compensation or marketing, said Zhao.

“Everyone has to be prepared,” Wang said. “Unfortunately, a lot of miners will eventually be driven out of the market.”