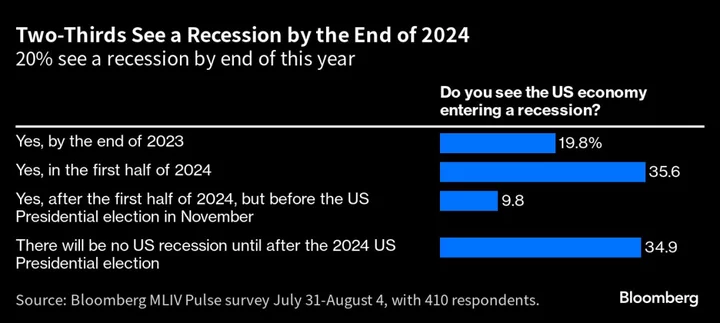

A clear majority of investors expect a US recession before 2024 is out, leading them to view the current bull market in stocks as ephemeral and to favor long-term US Treasuries.

That’s the takeaway from the latest Markets Live Pulse survey, which showed that roughly two-thirds of the 410 respondents anticipate a downturn in the world’s biggest economy by the end of next year. A minority of 20% of pollees even see a slump in 2023, at a time when the Federal Reserve’s own staff have ditched their recession forecast altogether.

Survey respondents appear to be looking past the economy’s current resilience and anticipating further damaging ripple effects from the Fed’s 5.25 percentage points of cumulative tightening over the past 16 months. The Fed lifted its benchmark rate to the highest in more than two decades last month and Chair Jerome Powell signaled additional hikes are possible.

The poll results are consistent with pricing in fed funds futures, which show traders expect the central bank to cut interest rates multiple times in 2024, by more than one percentage point in aggregate, ostensibly in response to eventual economic weakness.

The upshot is that investors see value in long-term Treasuries, with yields at one point last week threatening to test the multiyear highs touched in October. As they chart their allocation choices for the year ahead, survey respondents seem to be unbowed by last week’s bond-market slide, which came against the backdrop of the Treasury’s announcement that it will boost issuance, and as Fitch Ratings downgraded US sovereign debt. Treasuries recouped some ground Friday on data showing job growth in July was less than forecast.

Read More: Fitch Says Growing US Debt, Deficit Forecasts Spurred Cut

Investors are likely betting that the Fed will pivot to rate cuts in 2024, making long-maturity debt attractive despite the more than 1 1/4 percentage points of yield pick-up currently available on short-dated bills. Almost 60% of Pulse participants say now is a good time to buy Treasury securities with maturities longer than seven years. Of note, 59% of the responses came in before the Fitch downgrade on Aug. 1.

Still, the survey results signal a problematic backdrop for US stocks, which have roared higher in 2023, pushing the Nasdaq 100 to its best first half in history, thanks in no small part to an artificial intelligence-fueled surge. Market valuations have risen accordingly. The S&P 500 trades at a multiple of roughly 20 times earnings, where Yardeni Research data show that the 20-year average is closer to 16 times.

The biggest chunk of Pulse survey respondents, 47%, say the US stock market is a bubble powered by irrational exuberance, and a quarter view it as being in a bear market rally. Meanwhile, 28% say it’s a bull market that has more room to run.

Driving home the preponderance of bearish views the survey elicited, more than two-thirds of respondents say the S&P 500 is still mired in an earnings recession that has longer to run.

Another survey element underscores the complexity of the macroeconomic risks that investors must account for as they look to the year ahead.

Almost three quarters of poll respondents expect core inflation as measured by the personal consumption expenditures index — the Fed’s preferred inflation gauge — to either remain above 3% for the next 12 months, or to dip below that level but then rebound. It’s 4.1% now, the lowest since 2021.

It’s a view that stands in contrast to both the bullish survey response on long-maturity Treasuries and to market bets on rate cuts kicking in next year. And it suggests that many expect such a severe economic downturn at some point that the Fed will be easing policy even though inflation remains elevated. Hence the worries about equities.

The MLIV Pulse survey of Bloomberg News readers on the terminal and online is conducted weekly by Bloomberg’s Markets Live team, which also runs the MLIV blog. This week’s survey focuses on unlimited Paid Time Off (PTO). Is this the future of work and how will it impact companies? Share your views here.