Oil edged higher after posting the biggest loss in five weeks as traders took stock of a broad shift away from risk assets that countered signs of a tighter global crude market, including a record drop in US inventories.

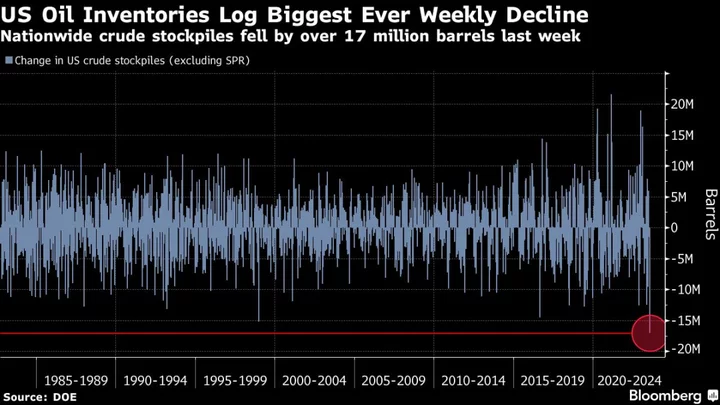

West Texas Intermediate rose toward $80 a barrel after tumbling by 2.3% on Wednesday as a spike in Treasury yields and the US dollar hurt equities and commodities. Crude’s sell-off came even as data showed a drop of more than 17 million barrels in US crude stockpiles, the biggest-ever draw in volume terms. Inventories at the key hub at Cushing shrank for a fifth week.

“While it was the largest-ever fall in volume terms, it was viewed as an anomaly due to adjustment factors the EIA uses,” analysts at ANZ Group Holdings Ltd. including Adelaide Timbrell said in a note, referring to the Energy Information Administration. “Even so, it highlights the tightness in the market that is emerging amid falling OPEC output.”

Crude rallied last month, with WTI erasing year-to-date losses, after the Organization of Petroleum Exporting Countries and allies cut production. The surge had lifted prices to the highest since April, spurring concerns there could be a pullback after such a rapid gain. The drop on Wednesday followed a downgrade of US credit by Fitch Ratings that hurt wider market sentiment.

“Despite a sharp drawdown in inventories, crude fell on a broader risk-off tone,” said Charu Chanana, market strategist at Saxo Capital Markets Pte in Singapore. The focus was on macro concerns after Fitch’s downgrade of the US and Treasury funding, which pushed US yields and the dollar higher, she said.

On Friday, the OPEC+ Joint Ministerial Monitoring Committee is due to hold an online review of the market to gauge the impact of the supply reductions that have been led by leading member Saudi Arabia and its ally Russia.

To get Bloomberg’s Energy Daily newsletter direct into your inbox, click here.