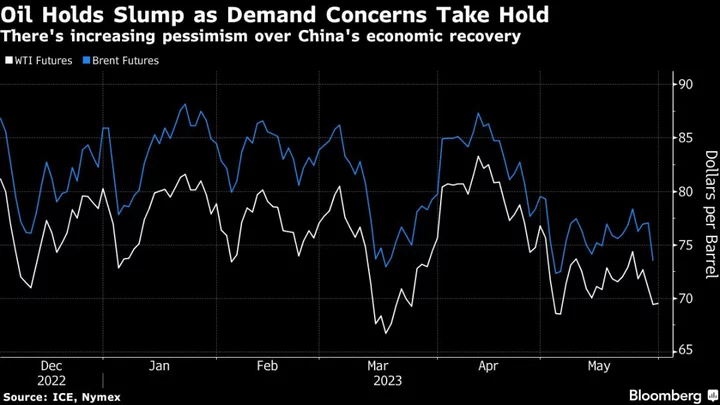

Oil held its biggest decline in four weeks on signs of weaker demand and sufficient supply ahead of an upcoming OPEC+ meeting.

West Texas Intermediate traded near $69 a barrel after settling 4.4% lower on Tuesday from Friday’s close. China’s manufacturing activity showed more signs of weakening in May, adding to concerns over the outlook for demand from the world’s biggest crude importer. The US dollar also rose, making commodities priced in the currency more expensive for international investors.

“Markets are worried that China’s commodity demand is weakening more quickly than anticipated,” said Vivek Dhar, director of mining and energy commodities research at Commonwealth Bank of Australia. “Views that OPEC+ may not look to cut oil production” also weighed on prices, he added.

OPEC+ is scheduled to meet over the weekend to discuss the group’s output policy, and most market watchers expect the coalition to keep production unchanged. Fundamentals don’t support the case for curbs, but a weak macroeconomic environment does, according to Standard Chartered Plc. RBC Capital Markets LLC also said a “lean cut” could be considered.

Oil is down around 14% this year as China’s lackluster economic recovery and tighter monetary policy from the Federal Reserve weighed on the demand outlook. More recently, concerns around the US debt ceiling have added to bearish sentiment, although there are signs of a possible resolution.

To get Bloomberg’s Energy Daily newsletter direct into your inbox, click here.

The prompt spread for WTI and Brent — the gap between the two nearest contracts — are holding in contango, when nearer futures trade at discounts to longer-dated ones. North Sea dated-to-frontline swaps, another gauge of physical market health, are at their lowest in over two months.