By Howard Schneider

The Federal Reserve held its benchmark overnight interest rate steady at its Sept. 19-20 policy meeting. New data will shape whether the U.S. central bank continues to stand pat at its Oct. 31-Nov. 1 meeting or proceed with another rate increase.

The Fed's target policy rate has been raised to the 5.25%-5.50% range from near zero in March of 2022, and inflation measured by the Fed's preferred personal consumption expenditures price index (PCE) was 3.5% in August, compared to a peak of 7% last summer.

Fed Chair Jerome Powell has said the pieces of the low-inflation "puzzle" may be aligning, but he does not trust it yet.

Here is a guide to some of the numbers shaping the policy debate:

JOB OPENINGS: (Released Oct. 3, next release Nov. 1)

Powell keeps a close eye on the Labor Department's Job Openings and Labor Turnover Survey (JOLTS) for information on the imbalance between labor supply and demand, and particularly on the number of job openings for each person without a job but looking for one. In August that key ratio clung to its downward trend as the Fed's rate hikes have slowed labor market demand. It's now about 1.5-to-1, compared with the nearly two jobs for every person seeking work during most of 2022. Levels around 1.2 were considered tight for the U.S. labor market before the pandemic.

INFLATION (Released Sept. 29, next release Oct. 12):

A key inflation measure fell in August, adding to what many economists feel is likely to be a steady disinflation. The PCE price index, stripped of volatile food and energy costs, rose 3.9% on a year-over-year basis compared to 4.3% in July, and recent month-to-month increases have averaged close to the Fed's 2% target. The headline rate did increase slightly, from 3.4% to 3.5%, but largely on the basis of energy costs. The Fed uses the PCE measures to set its 2% inflation target, but the decline in the "core" measure will be seen as evidence of slower price increases ahead.

Consumer price inflation rose for the second straight month, to 3.7% in August versus 3.2% in July. But the rise was largely the result of higher gas prices, which can be volatile and which Fed officials discount in analyzing price trends. More important to the central bank, underlying "core" inflation stripped of energy and food costs continued its decline, falling to 4.3% on a year-over-year basis compared to 4.7% in July.

While the overall picture is somewhat mixed, the inflation data in recent months likely doesn't change the policy outlook. But it does highlight the time it may take for Fed officials to be confident in a continued inflation decline.

INFLATION EXPECTATIONS (Released Sept. 29, next release Oct. 13)

Consumers' estimates of what inflation will average over the next 12 months and the next five years fell notably in September, the University of Michigan reported. At the one-year horizon, the inflation expectation fell to 3.2% from 3.5% in August. At five years, the reading fell to 2.8% from 3.0%.

The declines will be comforting to Fed officials who worry that rising inflation expectations can make consumers act in ways that will keep actual inflation higher. The one-year rate, notably, is now around its 40-year average.

RETAIL SALES (Released Sept. 14, next release Oct. 17):

Retail sales rose more than expected in August, increasing 0.6%. While that was largely due to higher gasoline prices, a separate measure of sales more directly related to economic output also rose slightly even though economists expected it to decline. Even as prior months' sales were revised lower, the August report showed household spending likely still adding to overall economic growth that has been on the central bank's radar as an inflationary risk.

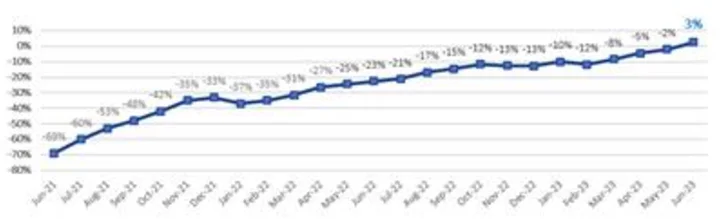

PRODUCER PRICES (Released Sept. 14, next release Oct. 11)

The producer price index (PPI) for August jumped 0.7%, the largest monthly increase since the peak of the Fed's inflation worries in June of 2022. Goods prices spiked a full 2%, another reason the central bank will be reluctant to declare its inflation battle over. Yet much of that was due to a jump in fuel prices, the sort of thing the Fed will discount. An index of service industry prices rose just 0.2%, and a measure of retailer and wholesaler margins fell, reinforcing arguments that inflation should continue to fall.

EMPLOYMENT (Released Sept. 1, next release Oct. 6):

The U.S. economy added 187,000 jobs in August, more than economists expected, in a sign of continued labor market strength. But the August report also contained more than a little evidence that a slowdown is underway. Prior months' gains were revised lower, with June job growth showing just 105,000 positions added, while the unemployment rate rose to 3.8% from 3.5% as more people joined the labor market.

Hourly wages grew at a brisk 4.3% on a year-over-year basis, but just 0.2% on a monthly basis, the smallest such jump this year.

Investors viewed the overall data as leaning against any further Fed rate increases.

BANK DATA: Released every Thursday and Friday

To some degree the Fed wants credit to become more expensive and less available. That is how increases in its policy rate influence economic activity. But bank failures in the spring threatened broader stress in the industry and a worse-than-anticipated credit crunch. Weekly data on bank lending shows bank credit has fallen on a year-over-year basis since the middle of July.

Bank borrowing from the Fed spiked around the failure of Silicon Valley Bank, but has declined since.

(Reporting by Howard Schneider and Ann Saphir; Editing by Andrea Ricci)