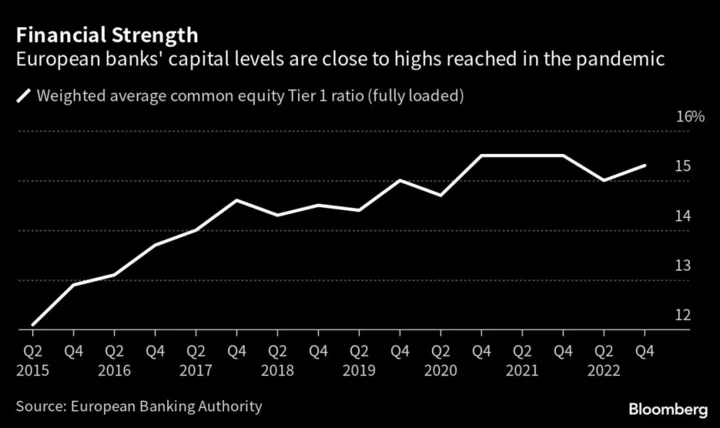

Many large European banks are emerging from early rounds of a key stress test in robust financial health, prompting some regulators to question whether to push harder at a time when investors are focused on the industry’s resilience.

Initial submissions to the European Banking Authority’s biennial assessment show several lenders’ capital ratios are higher than in previous exercises under the so-called adverse scenario, people with knowledge of the matter said, asking to remain anonymous as the submissions are private. That’s prompting the EBA and European Central Bank to lean on banks to be more conservative in subsequent rounds of the tests, which are set to conclude at the end of July.

The EBA assessment is a key exam for lenders because it gives insight into their preparedness to weather shocks and also feeds into their capital requirements. Banks, using data from the end of 2022, are tested under an adverse scenario and more benign baseline scenario for the three years through 2025. A clean bill of health strengthens the case for distributing billions of euros of capital to shareholders, even as economic uncertainty increases.

An EBA spokeswoman said it would be speculative to draw conclusions given the assessment is still in progress.

The 44-member Stoxx Europe 600 Banks Index, a benchmark for the industry, fell 2.5% as of 11:41 a.m. in London. It has gained 6.1% this year.

Positive Results

The angst over positive results is another sign of the tricky moment for banks and their overseers. Higher interest rates have been a boon for the banking industry overall, but the rapid speed of rate hikes caught some smaller US lenders unprepared, with disastrous consequences for those firms. European banks want to reward their shareholders after years of lean returns; regulators are wary of letting lenders get too confident.

“The European banking sector appears resilient to the challenges it has faced up to this point,” Anneli Tuominen, a member of the ECB’s Supervisory Board, said in a speech last week. “Nevertheless, we must not forget that there is still a lot of uncertainty.”

The ECB and other supervisors use the results of the stress tests to help set banks’ capital requirements. Faring badly can reduce a firm’s ability to make payouts or face regulatory pressure to cut them.

During the process it’s customary for authorities to challenge banks on preliminary submissions, requesting adjustments. While the central assumptions of the scenarios remain unchanged, some bankers have the impression that the regulators expected a bigger theoretical hit to capital ratios, people with knowledge of the matter said.

The EBA test covers about three quarters of banking assets in the European Union and Norway, with 70 banks calculating how they would fare following a hypothetical worsening of geopolitical developments, higher commodity prices and pandemic resurgence.

Agreed Methodology

An ECB spokeswoman declined to comment. The EBA said that it’s following the agreed methodology against the adverse scenario put forward by the European Systemic Risk Board, a fellow authority.

The adverse scenario would see elevated inflation and a global recession as well as increased interest rates. That would lead to a contraction in real economic output of 6% over three years, more severe than in previous tests.

The banks are faring better thanks to higher capital ratios at the start of the exercise than in the past, the benefit to earnings from rising interest rates and an improvement in the quality of their loan books, the people said.

The EBA’s last test, held in 2021, counted 50 banks that saw their high-quality capital depleted by a combined €265 billion ($286 billion). The firms’ had a starting common equity Tier 1 ratio of 15% and saw that trimmed to 10.2% in the adverse scenario.

(Updates with ECB official comment in seventh paragraph)

Author: Nicholas Comfort, Steven Arons, Sonia Sirletti and Jan-Henrik Förster