Bond traders are stepping up wagers that the Federal Reserve will steer the US economy into a recession.

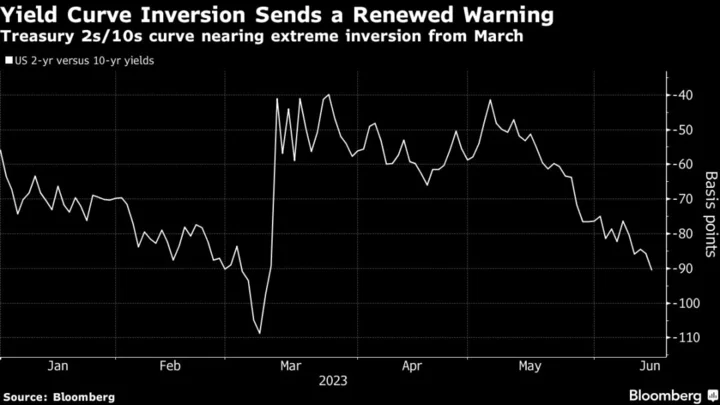

Policy-sensitive front-end Treasuries sold off Wednesday, while longer-date bonds rallied, after Fed officials indicated that they’re prepared to raise interest rates by another half-point this year following the first pause in the central bank’s 15 month hiking campaign. That sent the yield-curve inversion, as measured by the gap between two- and 10-year securities, to more than 90 basis points — a level last seen in March — and approaching this cycle’s 109 basis point extreme.

The price action suggests bond traders are skeptical that policymakers can avoid a so-called hard landing as they continue to press the case for higher borrowing costs in an effort to get a handle on inflation that remains more than double their 2% target.

“The Fed runs the risk of solving one policy error of being too easy for too long with another policy error as they ignore the growing credit contraction and persistent losses from higher rates,” said George Goncalves, head of US macro strategy at MUFG. “The catch-22 is that for them to ease, something now has to break or the economy has to crack.”

It’s not just bond traders who are growing concerned.

Sixty-one percent of respondents in a Bloomberg poll of terminal users conducted in the hours after the Federal Open Market Committee decision said tighter monetary policy will ultimately cause a recession at some point in the next year.

“The Fed was clearly trying to send a hawkish message that they are not quite done yet and don’t think they have made enough progress on inflation,” said Michael Cudzil, portfolio manager at Pacific Investment Management Co. “You see curve flattening and rates not pricing in the full extent of hikes, so the thinking is that these hikes may bite and the Fed is closer to the end.”

Officials left their target range for the federal funds rate unchanged at 5% to 5.25% Wednesday, but projected the key rate will rise to 5.6% by the end of this year, implying two more quarter-point increases, up from 5.1% in March. They also revised higher estimates of core inflation for year-end to 3.9%, from 3.6%, owing to what Chair Jerome Powell called surprisingly persistent price pressures.

Still, markets aren’t convinced borrowing costs will rise as high as central bankers project.

The highest rate on swap contracts for future meetings by late Wednesday was about 5.27% in September, with the one for July at 5.26%, compared to a current Fed effective rate of 5.08%.

Read More: Gundlach Doesn’t Think the Fed Will Resume Rate Hikes Soon

The Fed’s aggressive outlook for rate hikes through year-end may be an effort to dash bond-market expectations for cuts in the months ahead, according to Michael de Pass, global head of linear rates at Citadel Securities.

“We’re all in a wait and see mode, and the Fed is likely trying to stop the bond market from pricing in cuts immediately after they stop hiking,” de Pass said. “As the economy evolves, the Fed reaction function and how the market should trade will become clearer.”

For now, investors are left to parse incoming data, much as officials themselves say they’ll be doing.

Many bond investors have gravitated to steepener trades in recent months, driven by predictions that the Fed was largely done tightening and that policy easing was around the corner. Those wagers will be challenged should inflation and labor market data prove more resilient than expected in the coming months.

“Here we have the Fed saying we need to be restrictive and stay more restrictive for longer,” Jay Barry, co-head of US rates strategy at JPMorgan, said on Bloomberg TV after the decision. “That’s going to affect the front-end more, while the long-end is more impacted by the trend growth rates. I’m not necessarily surprised we’re seeing the yield curve invert further, if the Fed is saying we have to be more restrictive and stay there for a longer period of time, while there’s nothing to make us think that neutral interest rates or trend growth rates are actually higher.”