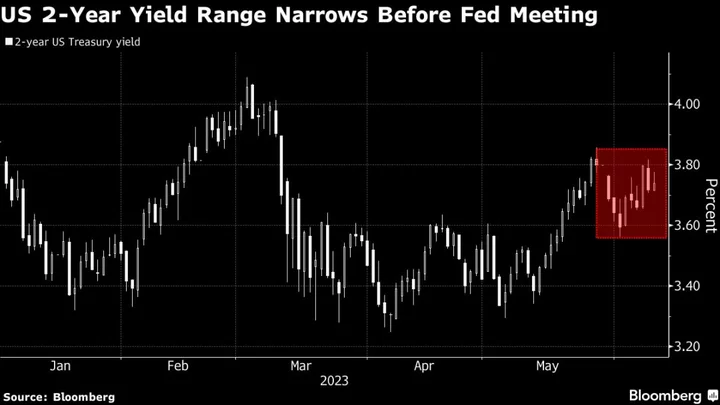

The risks for bond investors from next week’s Federal Reserve meeting go well beyond whether officials decide to raise interest rates again.

For a market that’s been betting that the central bank will pivot to cutting rates fairly soon, its updated quarterly forecasts for the policy rate and key economic indicators — set to be released Wednesday at the same time as the rate decision — will be at least as important.

The rate decision is critical of course, especially as traders remain split over whether an increase is likelier in June or July. But there’s more riding on the course of policy after that point.

The Fed’s been adamant that it’s premature to think about rate cuts this year, and traders no longer expect more than one. Still, there are plenty of bets in options and elsewhere that an economic slowdown will require lower borrowing costs.

So the economic projections of the Federal Open Market Committee members and Chair Jerome Powell’s tone during his post-decision press conference may shape the response more than the timing of the next quarter-point hike. If they suggest that conditions are peaking, wagers on a pivot would increase, while a more robust and hawkish set of predictions would spur bets on higher-for-longer rates.

“The market is positioned for a rally in long duration,” said Meghan Swiber, rates strategist at Bank of America Corp., referring to the part of the market that benefits most from declining yields, “and the ultimate thing that underpins that view is that the Fed is done with the hiking cycle.”

Asset managers favoring long-maturity Treasuries or positioning for a steeper yield curve are anticipating the end of Fed rate increases, Swiber said. Bank of America’s latest monthly survey of investor sentiment found that exposure to US dollar duration is at its highest level since 2004, having eclipsed the pandemic highs of April 2020.

Swap contracts linked to future Fed meetings — which at the end of May almost fully priced in a quarter-point increase in June — have downgraded that outcome to about one in three — still an unusual lack of consensus so soon before the event. The Fed has raised rates 10 consecutive times since March 2022, and in all but two cases swaps pricing reflected little doubt about the likely outcome.

The July contract’s rate at about 5.31% is about 23 basis points higher than the 5.08% level of the rate targeting by the Fed, nearly fully pricing in a 25-basis-point increase by then. For December, the contract rate is 5.07%, anticipating that any quarter-point rate increase from the current level will be reversed by year-end.

“The Fed is pretty much done even if they go one or two more times,” said Arvind Narayanan, senior portfolio manager at Vanguard Group Inc. “Either the economy slows materially into a recession that forces the Fed to cut rates, or the economy slows down enough to keep rates at 5% for the rest of year and then the Fed slowly eases next year.”

What Bloomberg’s strategists say

“It’s rare indeed for the Fed to re-tighten policy after pausing. It’s even rarer for it to do so when rates are already restrictive.”

— Simon White, macro strategist

For the full column, click here

Inflation data to be released early Tuesday may prove decisive. The growth rate for the consumer price index is forecast to slow to 4.1% in May from 4.9%, and to 5.2% from 5.5% excluding food and energy. The Fed seeks an inflation rate averaging 2% over time.

Citigroup Inc. economists, who expect a June rate increase, pin that forecast on May CPI readings they predict will show underlying inflation remains closer to 5%, Andrew Hollenhorst, chief US economist at the bank, said in a video released Thursday.

Ahead of the meeting, signals from the Treasury market may be distorted by an unusually large amount of new supply compressed into two days. In addition to the monthly sales of 3- and 10-year note and 30-year bonds, normally spread over three days, $206 billion of Treasury bills are slated to be sold to replenish the government’s coffers, which were depleted until the federal debt limit was suspended last week.

Expectations for more Fed rate increases peaked this year in early March, when Powell said policymakers were prepared to re-accelerate the pace of rate increases if warranted by economic data. The two-year Treasury note’s yield, more sensitive than longer maturities to changes in the Fed’s rate, briefly topped 5%. It’s stabilized around 4.6% as the case for more rate hikes has been dented by several regional bank failures and other signs that the economy may finally be reckoning with tighter financial conditions.

“We think it’s more likely the Fed will skip into July,” said Thomas McLoughlin, head of fixed income for the Americas in the chief investment office at UBS Group’s wealth-management arm. “But Powell’s message has been that his intent is to keep a tight monetary policy at least through the end of the year and potentially into next year.”

What to Watch

- Economic data calendar

- June 12: Monthly budget statement

- June 13: Consumer price index; NFIB small business optimism

- June 14: MBA mortgage applications; producer price index

- June 15: Retail sales; jobless claims; import and export price indexes; Empire manufacturing; Philadelphia Fed business outlook; industrial production; business inventories; Treasury international capital flows

- June 16: New York Fed services business activity; U. of Michigan sentiment and inflation expectations

- Federal Reserve calendar

- June 14: FOMC policy decision; summary of economic projections; Chair Jerome Powell press conference

- Auction calendar

- June 12: 26- and 13-week bills; 3- and 10-year notes

- June 13: 52-week bills; 42-day cash management bills; 30-year bonds

- June 14: 17-week bills

- June 15: 4- and 8-week bills